Futures Market: Overnight, LME copper opened at $9,184/mt, dipped to $9,170/mt at the beginning of the session, then climbed steadily, peaking at $9,243/mt near the close and finally settling at $9,237/mt, up 0.02%. Trading volume reached 16,000 lots, and open interest stood at 296,000 lots. Overnight, the most-traded SHFE copper 2503 contract opened at 75,200 yuan/mt, dipped to 75,110 yuan/mt initially, then fluctuated upward, peaking at 75,450 yuan/mt near the close and finally settling at 75,390 yuan/mt, up 0.25%. Trading volume reached 21,000 lots, and open interest stood at 160,000 lots.

【SMM Copper Morning Brief】News: (1) US President Trump stated that he would demand the US Fed to cut interest rates immediately and urged Saudi Arabia and OPEC to lower oil prices.

(2) Initial jobless claims in the US for the week ending January 18 recorded 223,000, slightly above the market expectation of 220,000 and higher than the previous value of 217,000.

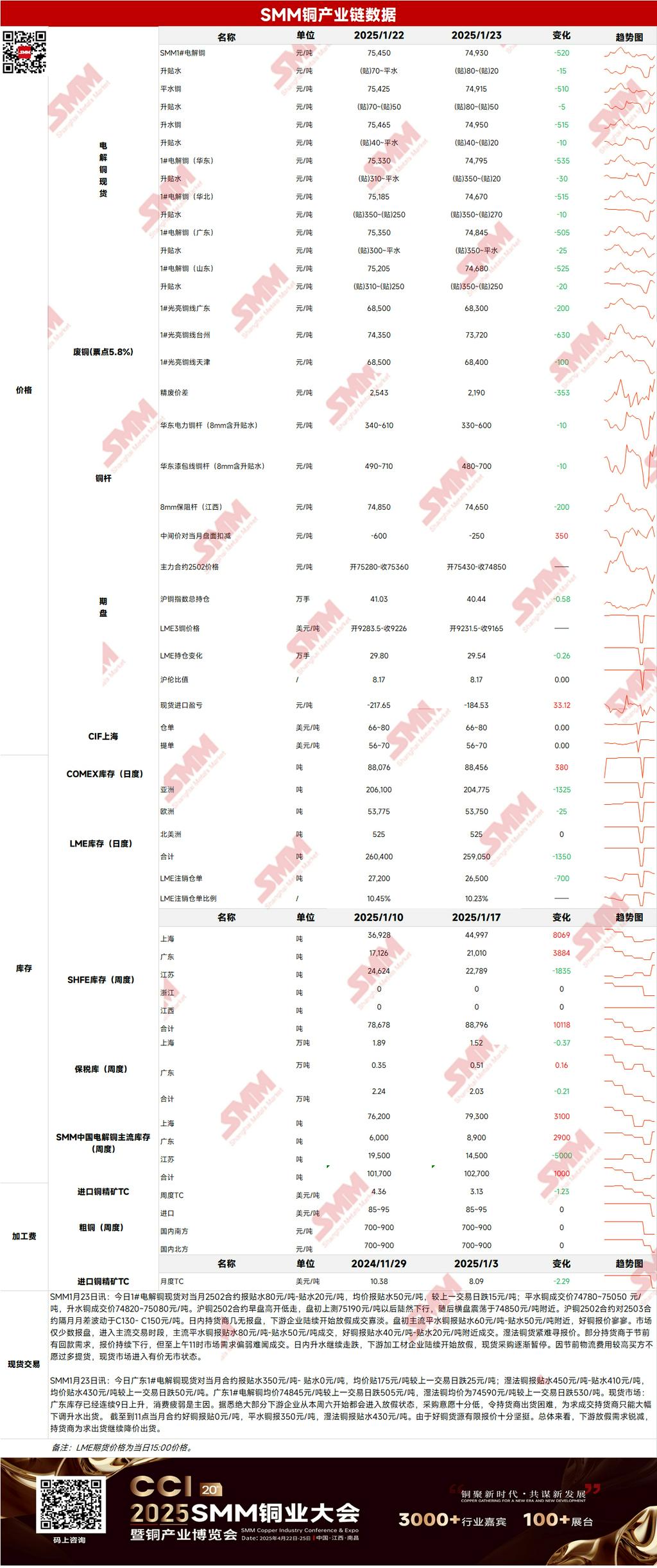

Spot Market: (1) Shanghai: On January 23, #1 copper cathode spot prices against the front-month 2502 contract were quoted at a discount of 80-20 yuan/mt, with an average discount of 50 yuan/mt, down 15 yuan/mt from the previous trading day. Spot premiums continued to decline yesterday as downstream processing enterprises gradually began their holidays, and spot procurement slowed. Due to high pre-holiday logistics costs, buyers were reluctant to pick up goods, leading the spot market into a state of nominal prices without transactions.

(2) Guangdong: On January 23, #1 copper cathode spot prices against the front-month contract were quoted at a discount of 350-0 yuan/mt, with an average discount of 175 yuan/mt, down 25 yuan/mt from the previous trading day. Overall, downstream demand plummeted as enterprises went on holiday, and suppliers continued to lower prices to facilitate sales.

(3) Imported Copper: On January 23, warehouse warrant prices were $66-80/mt, QP February, with the average price unchanged from the previous trading day. B/L prices were $56-70/mt, QP February, also unchanged. EQ copper (CIF B/L) was quoted at $6-20/mt, QP February, with the average price unchanged, referencing cargoes arriving in late January and early February. Yesterday, the SHFE/LME price ratio against the SHFE copper 2502 contract was around -490 yuan/mt. LME copper 3M-Feb was at C$75.09/mt, and the 2502-2503 month-date spread was around C$36/mt. The near-month price ratio improved slightly yesterday, and bonded zone arrivals increased slightly. However, overall market activity remained sluggish as most participants began their holidays, making transactions scarce.

(4) Secondary Copper: On January 23, secondary copper raw material prices remained unchanged MoM. Guangdong bare bright copper prices were 68,400-68,600 yuan/mt, unchanged from the previous trading day. The price difference between primary metal and scrap was 2,543 yuan/mt, down 250 yuan/mt MoM. The price difference for secondary copper rods was 715 yuan/mt. According to the SMM survey, secondary copper rod enterprises have gone on holiday, and transactions were lackluster yesterday.

(5) Inventory: On January 23, LME copper cathode inventory decreased by 1,350 mt to 259,050 mt. SHFE warehouse warrant inventory increased by 2,948 mt to 20,367 mt.

Prices: Macro side, Thursday's data showed that US initial jobless claims rose only slightly last week, indicating steady employment growth in January. Meanwhile, Trump questioned Fed Chairman Powell's rate decisions, demanding an immediate interest rate cut and calling for global emulation. This led to a weaker US dollar. However, as Trump has yet to make a clear statement on tariff issues, copper prices saw only a slight increase. Fundamentals side, with the Chinese New Year approaching, downstream processing enterprises have gradually begun their holidays. Additionally, high pre-holiday logistics costs deterred buyers from picking up goods, leading the spot market into a state of nominal prices without transactions and sluggish market activity. As of Thursday, January 23, SMM copper inventories in major regions across China increased by 17,400 mt from Monday to 127,200 mt, up 19,100 mt from last Thursday. Compared to Monday's inventory changes, most regions saw an increase, except for a slight decline in Jiangsu. Total inventory was 42,000 mt higher than the 85,200 mt recorded YoY. In terms of prices, macro policies remain unclear, coupled with sluggish spot market transactions, making it unlikely for copper prices to rise further today.

》Click to View the SMM Metal Database

【The above information is based on market data collected and comprehensive evaluations by the SMM research team. The information provided herein is for reference only and does not constitute direct investment advice. Clients should make prudent decisions and not substitute this information for independent judgment. Any decisions made by clients are unrelated to SMM.】

![Macro Sentiment Wavered, BC Copper Closed Flat After Wide Intraday Swings [SMM BC Copper Commentary]](https://imgqn.smm.cn/usercenter/GfvuY20251217171708.jpg)